There has never been a better time for investors to hold a 60:40 portfolio, according to Liontrust's head of multi asset John Husselbee, despite the poor performance of such strategies last year.

Husselbee (pictured) has been working in the industry since the mid-1980s but described 2022 as “one of the most humbling and painful years” he has experienced in his career.

He said that as a multi-asset manager, it was not difficult to see why: in the past 100 years, 2022 was only the fourth time that bonds and equities both lost money.

“In the past 20 to 25 years, lower-risk investors always had the protection of bonds in the most stressful moments for markets as they were a diversifier with a low correlation to equities,” he said.

“Whether you were looking at the TMT [technology, media and telecom] bubble or the global financial crisis, in those periods, bonds bailed you out.

“However, that simply wasn't the case in 2022. We had a period where equities went through that risk-off moment and you were looking for bonds to provide that protection, but it basically just disappeared. And in some cases, bonds underperformed equities.”

Such poor performance for bonds, coming at a time when equities also fell, has led many commentators to claim the 60:40 portfolio is no longer fit for purpose.

However, Husselbee said that these critics were looking at it from the wrong perspective. He pointed to data showing that over the past 30 years, using the MSCI World index as a proxy for equities, there have been just two occasions when a negative year was followed by another negative year (1999 and 2000).

For bonds, using the Bloomberg Global Aggregate index as a proxy, there was only one occasion when this happened – 2011.

“We've seen a significant repricing in bond yields,” Husselbee continued. “We've seen a significant repricing in equities as well.

“And if there was ever a time for 60:40 to work, if there was ever a time to get above-average returns over the long term for 60:40, it’s when yields are high and equity valuations are low.”

Husselbee said that one of the reasons why some commentators may be shying away from the these ‘balanced’ portfolios is that this is the first time they have seen yields and interest rates this high and may be under the impression that this is in some way abnormal.

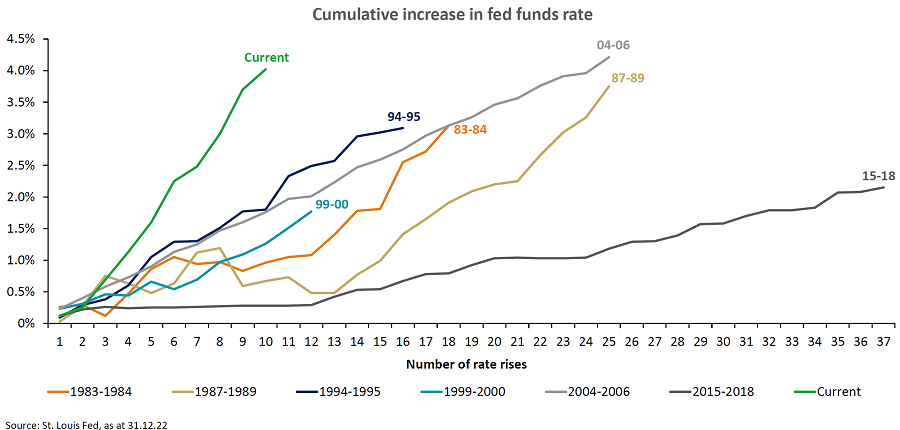

However, the manager said the current environment more closely resembles typical financial conditions than the post-financial crisis period, adding the only thing abnormal about it is the “fast and furious” way central banks have tightened conditions. For example, he noted the Federal Reserve raised rates by 4 percentage points in just seven months, when such an increase would usually take two to three years.

However, he said this spike has suddenly made bonds attractive once more, while the volatile macroeconomic backdrop has created further opportunity to add value.

“When we talk about repricing, we have to talk about the repricing of geopolitical risk because it's back on the table,” he continued.

“Over many, many years, we've had a world that has been fairly peaceful: globalisation has encouraged collaboration. However, following the election of [US president Donald] Trump, America and China have begun to lock horns over tariffs and various other issues and that was the starting point of a contraction in globalisation – the war in Ukraine is just an acceleration of that.”

Husselbee said major markets are already beginning to behave more independently of one another on issues such as energy and food security. Next, he said there is likely to be more of a divergence in monetary policy, with one major central bank tightening just as another starts loosening.

“Of course, we've seen that in the past, but it was in a more collaborative way. Now I think it's going to be more independent,” he said, before adding: “If I were a bond manager who had just enjoyed a 30- to 35-year bull market, I might have thought, ‘okay, that's the time to hang up my boots’.

“But one year on I would probably be thinking ‘hang on a minute, there are some fantastic opportunities here’, because my market has just been repriced back to yields I haven't seen for the past 10 years, the world is beginning to contract, central banks are becoming more independent of each other and I've got a wider opportunity set.

“It is a pretty exciting time for bond managers again.”