Technology has been the dominant sector for the past 15 years and this may well continue thanks to the strong interest for artificial intelligence (AI) investors showed last year.

The outperformance of the sector has benefited tech-specialist Polar Capital Technology Trust, which has been one of the best performing investment trusts of the past decade and was one of the few close-ended funds to beat the Nasdaq index last year.

Below, portfolio manager Ben Rogoff explains why the tech sector could continue to outperform in the future, why he hasn’t taken profit yet from his AI stocks and why contrarianism is not rewarding in his field.

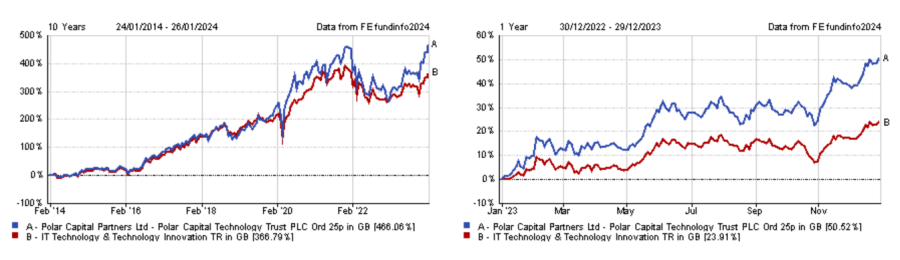

Performance of trust over 10yrs and in 2023 vs sector

Source: FE Analytics

Could you explain your investment process?

It is about identifying key themes and trying to ensure that we capture them for our investors in the portfolio.

We try to focus on large market opportunities rather than exciting niche applications. Our philosophy is that returns within tech are generally generated by a few companies. Therefore, it's critical for us to participate in their success. Moreover, we think public markets do a very poor job in pricing ‘blue sky’, binary stocks, so we tend to avoid those companies.

We also revisit stocks that haven’t acted well, because we might have got them wrong and either exited or reduced our exposure. But we don't buy more of something just because it's cheaper than when we bought it last.

Why should investors have a pure technology play in their portfolio?

The information technology sector accounts for 29% of the S&P 500, so you can invest in a US fund to get exposure to it, but you will be diluted by other sectors.

The reality is that tech is coming after some of those other sectors. If you've invested in advertising businesses or retailers alongside tech over the past 20 years, you have been caught off by e-commerce and advertising companies such as Google or Amazon.

However, the key when investing in a single theme is to make sure you understand that it is inherently more volatile than investing in a broader market fund.

Technology outpaced every other sector in the 2010s, which was a low inflation period. Can it continue to outperform in an environment where inflation is structurally higher?

In theory, tech is a deflationary sector associated with falling prices. Therefore, it may not protect you well in an inflationary environment.

While the sector isn’t typically associated with inflation, there are a lot of monopolies within tech, which means those companies have pricing power. And if AI is as productive as we believe it is, there's going to be a lot of pricing capture in companies that can deliver productivity. Another point to make is that the sector itself is far less capital intensive than it used to be.

Tech mega-caps perceived as AI beneficiaries rallied last year. Do you think this can continue in 2024?

We describe ourselves as AI maximalists, as we believe it represents the next general purpose technology. It is one of those unique moments for the tech sector. We haven't really been taking profits in AI stocks. In fact, we've been adding to our AI exposure so far this year.

The ‘Magnificent Seven’ are all perceived to be on the right side of the AI trade, and just to be clear, we own them all. We estimate they can continue to move higher and there's no reason why they shouldn't participate in a decent market.

That being said, the return profile of last year is very unlikely to be repeated, because 2022 was pretty awful. You can't look at the performance of Nvidia on the way up in 2023 without looking at what it did in the prior year. The same is true for most of those stocks.

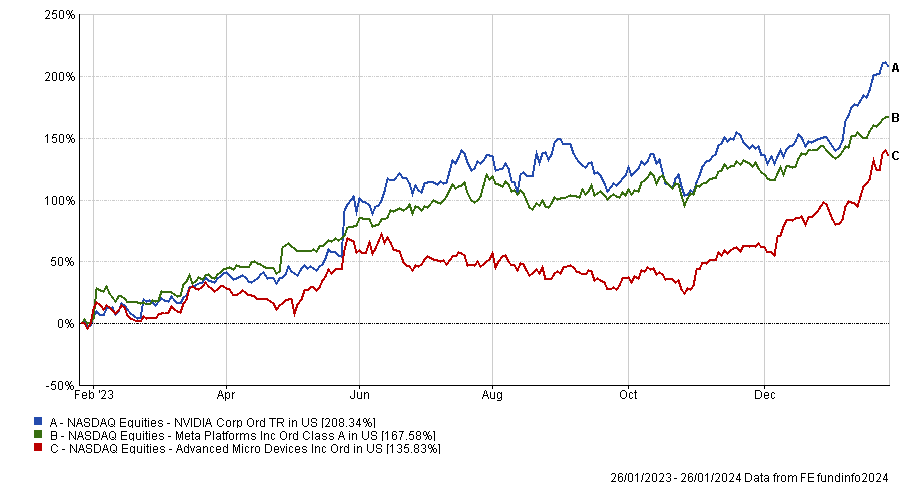

What have been the main contributors and detractors to performance over the past 12 months?

In absolute terms, Nvidia. It's been a phenomenal stock. We were broadly neutral for the full year and overweight during the latter half of the year. From a relative perspective, it didn't add very much, but it has been critical from an absolute one. Our best relative performer was Advanced Micro Devices.

Performance of stocks

Source: FE Analytics

Liquidity has been the single biggest drag to our performance. An average cash position of 4% or 5% in a market that's on fire is quite expensive. I tend to use cash as a way to try to soften the portfolio’s beta, but it’s nonetheless been the biggest detractor. From a relative perspective, the biggest single detractor was Meta. The stock surged last year, but we were underweight by about 70 basis points.

What do you do outside of fund management?

I've got a wife and two teenage sons, so I spend as much time with them as possible. I also manage the youth football team for one of my sons on weekends. That's quite time consuming.