After the turbulence and uncertainty that characterised 2022, there are now only two macro topics of significance – inflation and recession. On days when inflation leads the narrative, short-term government rates rise and risk-on sentiment strengthens, with equities and high-yield risk performing on the hope of a soft economic landing in the US.

When recession fears lead, the risk-off mood dominates and we typically see interest rates shift lower, government bonds perform and equities and high-yield spreads sell off.

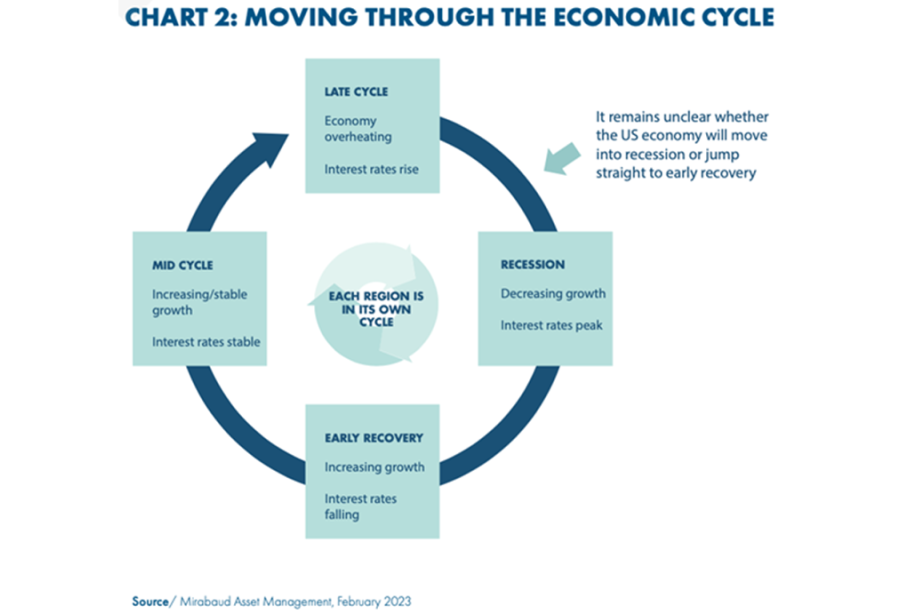

Currently, the market is particularly data dependant because the US economy is positioned between two stages of the economic cycle – ‘late cycle’ and ‘recession’. Either the Federal Reserve has tightened enough – or even over-tightened – and the US economy will rapidly enter recession, or it has done sufficient groundwork to facilitate a soft-landing and shift the economy towards the ‘early recovery’ stage.

We expect the macroeconomic landscape to remain turbulent and short-termist. Each new data point provides an immediate steer on market direction but cannot be relied upon to support a longer-term directional view. Being attuned and responsive to data is what will separate successful investors from the laggards.

Opportunity in high yield

High yield bonds currently offer genuinely high yields and low interest rate risk, while default rates are expected to remain below average. The asset class is set to deliver solid returns through to the end of the cycle, with the possibility of superior returns on a long-term view. There are several components to the high-yield opportunity.

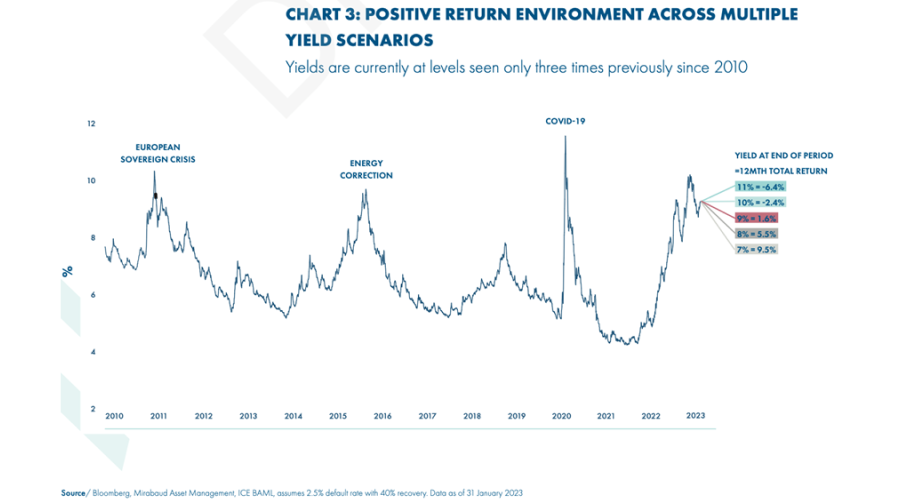

Firstly, the outlook for yields and spread levels is worth considering. Typically, when yields go above 8% in the high-yield universe, the asset class delivers positive forward returns on a 12-month view.

When yields exceed 9%, forward returns are generally strong. Spreads on the ICE BofA Global High Yield Index are currently in the 450-500bps range. In a typical recession, we would expect to see wides of about 700bps.

We forecast a shorter and shallower global recession, where spread widening should remain below 700bps. We also have higher interest rates than in prior cycles and any slowing would see this compress, offsetting some of this tightening. If we see a soft landing, spreads could go back to pre-crisis levels of 300-350bps.

The second component is credit quality. Pandemic-induced economic uncertainty has pushed corporates to conservatively manage balance sheets, resulting in an improved cost base and greater focus on leverage and cashflow generation. The weakest companies defaulted during 2020 and 2021, with those left largely representing good-quality, well-run businesses that can withstand a slowdown in growth.

Additionally, only 17.5% of the market is due to mature before 2025. There is no big maturity wall looming, as companies have refinanced to take advantage of years of low rates, extending their maturity dates. This means most corporates will not be forced to refinance at today’s elevated rates.

Lastly, default rates are close to historical lows and should remain below average through 2023. We are expecting 3-4%, reflecting the quality of the universe and the lack of a maturity wall. There are also no ‘stressed’ sectors that could trigger a default cycle, as we saw with housing in 2008 and energy in 2015.

A unique market environment

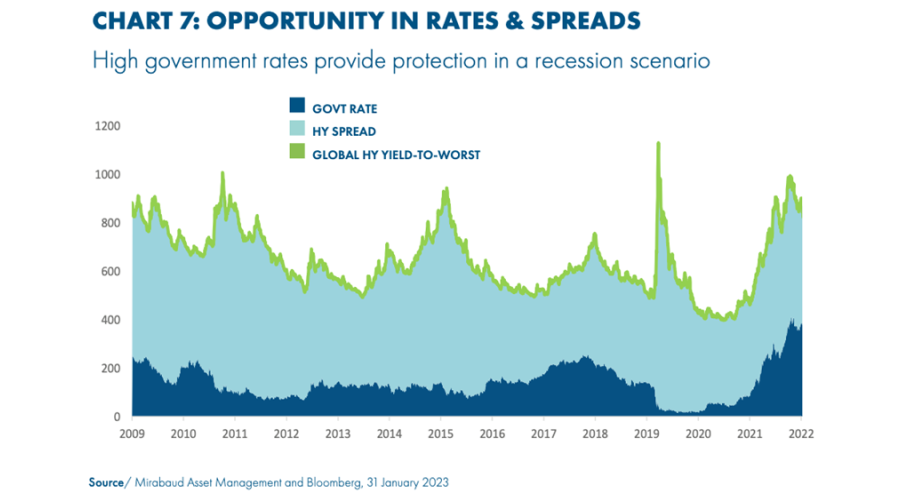

At the brink of most economic slowdowns, corporate fundamentals are typically already weak. But today’s high yield bond issuers are in much better financial shape than issuers entering past recessions thanks, in part, to years of low rates and an extended period of uncertainty surrounding the pandemic.

If we look at historically challenged times, high-yield spreads widen. But today, for the first time, we have a large government rates buffer. The yield on high yield is made up of the government rate plus the high-yield spread, so as spreads widen, it means the economy is slowing, the Fed will have reached its pivot point, and government rates will compress.

The total yield will be relatively unchanged, so even with a recession and wider spreads, you can still generate positive returns in high yield. We think the risk/reward trade-off is currently more favourable in high yield than in equities, as you still have double-digit upside in credit, but with much greater downside protection.

In a downturn, government rates go lower and this goes directly into the price of high yield bonds as a part of the yield. For equities, this often goes into the valuation multiple, but that would be dominated by the downgrade to earnings.

While markets will likely experience some near-term volatility, investors with a medium-term investment horizon should be able to take advantage of historically high yield levels to achieve attractive returns. We believe high yield should be considered a core fixed income allocation throughout the cycle.

Fatima Luis is a senior portfolio manager at Mirabaud Asset Management. The views expressed above should not be taken as investment advice.